Summer 2026: Why Now Is a Smart Time to Lock In Final Expense Coverage

Rates rise with every birthday. Here's why the slower summer months are a good window for seniors to compare carriers before the fall.

Final expense insurance is one of those purchases that’s easy to defer. Nothing’s on fire, the topic isn’t urgent, and there’s always next month. Summer is actually a strong window to handle it — partly because of how insurance pricing works, and partly because the broader season tends to be quieter administratively.

This isn’t a “limited time offer” pitch. There aren’t real seasonal discounts on final expense. But there are practical reasons summer is a sensible time to put coverage in place rather than waiting until fall or later.

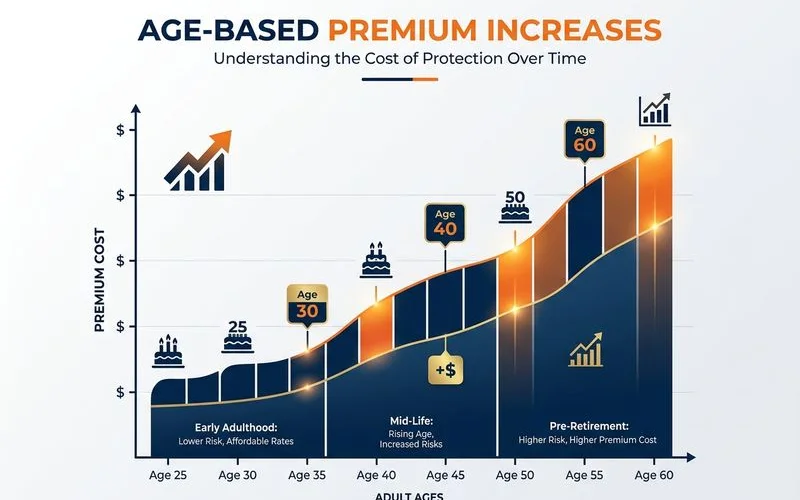

Premiums Rise With Each Birthday

The single most consistent driver of premium increase isn’t market timing or carrier pricing changes — it’s age. Whole life premiums are calculated based on your age at application. Each year of delay typically adds 2–4% to the lifetime cost of the same coverage.

For a 70-year-old considering a $10,000 policy at roughly $70/month, waiting 12 months to apply at age 71 typically adds $3–$5 per month. Over a 15-year horizon, that’s $540–$900 in extra premium for identical coverage.

If your next birthday is approaching, the math favors applying before it rather than after. Summer often falls between birthdays for buyers planning fall decisions — handling the application now, rather than waiting until “after the holidays,” locks in the current age-based rate.

The Health Stability Factor

The application process favors stable health. Underwriting wants to see no recent hospitalizations, no recent medication changes, no recent flare-ups of chronic conditions. Summer for many seniors is the most stable health window of the year — temperatures are moderate, flu season is over, seasonal allergies aren’t triggering respiratory issues.

By contrast, fall and winter bring:

- Higher rates of respiratory illness

- Flu and pneumonia hospitalizations

- COPD exacerbations from cold air

- Cardiac stress from holiday-season activity

Applying when health is stable means fewer underwriting follow-ups, faster approval, and a better chance at the higher rate class. Summer is often a clean window for this.

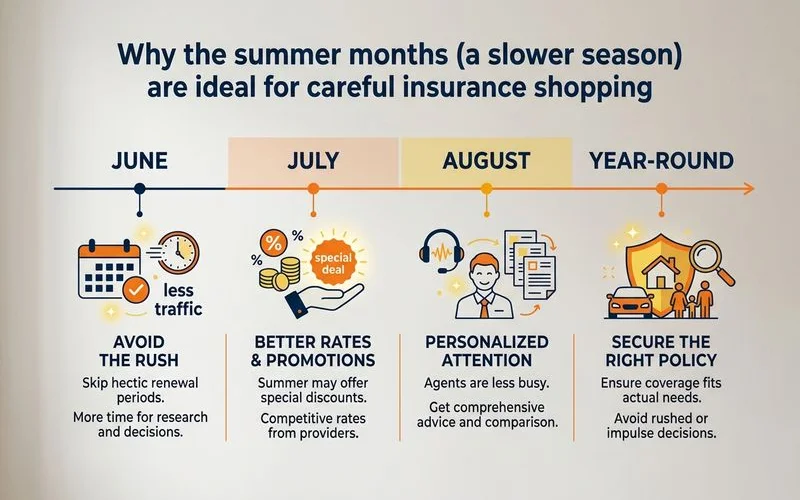

Administrative Bandwidth

Insurance carriers and independent brokerages run on calendar cycles like any business. Q1 (Jan–Mar) is the busiest quarter — open enrollment for other lines, year-end carryover, fresh-year buyer interest. Q4 (Oct–Dec) sees holiday-driven decision-making and family conversations.

Summer is the slowest stretch for most senior-life-insurance specialists. What that means for you:

- Faster response times from agents

- More attention to your specific case

- More time for thorough carrier comparison

- Fewer phone-tag delays during the application

If you’ve been putting off the shopping process because it feels like a chore, summer is genuinely the easiest time to get through it.

Why Not Wait Until Fall?

A few specific scenarios where waiting until fall makes sense:

- You’re undergoing a medical procedure or treatment that’s expected to resolve by fall (e.g., a planned surgery, completing a course of treatment that improves your underwriting profile)

- You’re quitting smoking and the 12-month non-tobacco reclassification window aligns with fall

- A specific carrier you’re waiting on has announced a product change taking effect later

In most other situations, the math favors not waiting. The birthday clock keeps ticking. Health profile changes are equally likely to worsen as improve. Carriers occasionally tighten underwriting tables, not loosen them.

What “Locking In” Actually Means

Whole life premiums are locked at the rate set at application — they don’t increase as you age. Once you’ve placed the policy at age 70, your premium stays the same at 75, 80, 85, and beyond. This is fundamentally different from term life, where rates can adjust at renewal.

Locking in this summer means locking in 2026 pricing for your current age, current health, current tobacco status. That rate stays with you for the life of the policy. Waiting means re-applying at whatever your age, health, and pricing tables look like later — which might be the same, but more often is more expensive.

A Reasonable Approach

If you’ve been thinking about putting coverage in place and don’t have a specific reason to wait:

- Get a free quote comparison this summer. It takes about two minutes to start the process. No medical exam required.

- Review the offers. A licensed independent agent will shop multiple A-rated carriers and report back which fits your profile best.

- Apply with the right carrier. Application usually takes 30–45 minutes, including the phone interview.

- Lock in the rate. Coverage is typically in force within 1–3 weeks.

Done by fall, with no pressure to navigate it during a busier season.

Ready to get a real number? — Get a free quote and we’ll show you what’s available now.

Prime Mutual Editorial Team

Final Expense Insurance Specialist (Former Licensed Life Producer)

Built on the firsthand experience of a former licensed life insurance producer who held an active life insurance license from 2011 to 2022.

✓ Former active life insurance producer license (2011-2022)

Ready to See What Fits Your Situation?

Free, no-obligation quote from a licensed independent agent. No medical exam.