We constantly review life insurance contracts for homeowners and business owners. The fine print in these policies dictates exactly what your family receives during a crisis.

Many people misunderstand the specific waiting periods attached to popular final expense plans. Our analysis shows a massive coverage gap between the two main options.

Let’s look at the data, what it actually tells us, and how you can respond. This guide breaks down exactly how simplified issue vs guaranteed issue coverage works.

The right choice saves you thousands of dollars.

The Critical Difference

The single biggest distinction between simplified issue and guaranteed issue is what your family receives if you pass during the early years of the policy. We see this scenario play out frequently in the industry. A clear understanding of the payout structure is vital:

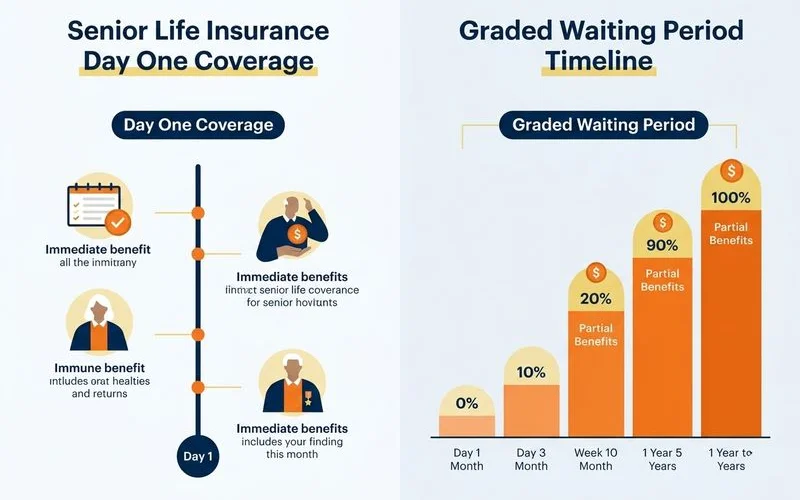

- Simplified issue: Full death benefit from day one. Even if you die in the first month, the beneficiary receives the full face amount as a tax-free lump sum.

- Guaranteed issue: Natural-cause deaths during the two to three-year graded period pay only a return of premium plus interest. Full benefits apply only after the waiting period.

The 2023 National Funeral Directors Association (NFDA) report places the median cost of a traditional funeral at $8,300. A cremation with viewing costs around $6,280. We calculate that a $10,000 policy with a waiting period might only pay out $1,500 if death occurs in the first year.

This leaves your family scrambling to cover a massive shortfall. That gap is the entire point of trying to qualify for a day one life insurance coverage policy.

What Qualifying Looks Like

To qualify for simplified-issue day-one coverage, you need to pass a short health questionnaire. These applications typically involve 10 to 15 simple yes or no questions, and our guide on how to qualify for simplified issue walks through them in detail. We find that most healthy adults in their 50s, 60s, and early 70s pass easily.

Insurance companies verify your answers behind the scenes. Carriers check the Medical Information Bureau (MIB) database to review your past insurance applications and prescription history. Our team always reminds clients that this electronic review is thorough.

It often catches omitted medical details instantly. Many manageable conditions still qualify for day one life insurance coverage. We regularly see approvals for applicants with the following health profiles:

- Controlled high blood pressure.

- Controlled Type 2 diabetes (sometimes Type 1, depending on the carrier).

- Past cancer history beyond the carrier’s lookback window (Mutual of Omaha typically uses a two-year lookback for cancer).

- Heart event over five years ago that remains stable.

- Multiple maintenance medications with no recent hospitalizations.

The “knockout” conditions will disqualify you from simplified issue at most carriers. We advise clients to check this list before applying:

- Active cancer treatment.

- Recent severe stroke or heart attack within the last 12 months.

- Dementia or Alzheimer’s diagnosis.

- Advanced COPD requiring continuous oxygen.

- Current residency in a nursing home or an assisted-living facility with ADL dependency.

If you can honestly answer “no” to the knockout questions, simplified issue is almost certainly available to you at some A-rated carrier. Our experience shows that many options exist for relatively healthy individuals.

Cost Comparison

Beyond day-one coverage, simplified issue typically costs significantly less than guaranteed issue. A clear price markup exists between the two tiers. We compiled this data to show the exact monthly difference:

| Profile (10k policy, age 65) | Simplified Issue | Guaranteed Issue |

|---|---|---|

| Healthy non-tobacco female | $50/mo | $80/mo |

| Healthy non-tobacco male | $60/mo | $95/mo |

| Tobacco user, 70 | $90/mo | $135/mo |

That is not a small pricing gap. Guaranteed policies charge a 50% to 60% premium markup across the board. Our calculations show the extra premium adds up to $5,000 to $8,000 over 15 years.

You pay thousands more for the exact same eventual coverage. This higher cost compounds the early-year benefit reduction. We want you to avoid paying more for an inferior product.

Why People Default Into the Worse Product

Mass-market advertising heavily promotes guaranteed issue because it requires no medical questions. The pitch sounds fast and simple on television. We notice that “easier to apply for” rarely translates to a “better product for you.”

A 2024 LIMRA consumer study revealed that 72% of Americans overestimate the true cost of life insurance. Over half of the respondents admitted they base their cost estimates on a wild guess. Our analysts see this confusion drive people toward heavily advertised, high-cost options.

Common Advertising Pitfalls

Smart shoppers watch out for these specific red flags in final expense commercials:

- Focusing only on the premium: Ads highlight a low monthly price but hide the tiny payout amount.

- Ignoring the waiting period: Commercials gloss over the mandatory two-year graded benefit window for natural deaths.

- Selling fear over facts: Pitchmen use high-pressure tactics instead of clearly explaining the policy limits.

Consider the popular $9.95 plan heavily promoted by Colonial Penn. This company sells guaranteed acceptance policies using a unit pricing structure. We warn clients about the fine print on these units.

For a 65-year-old male, a single $9.95 unit buys less than $900 in actual death benefit coverage. That payout barely covers the cost of a standard cremation. Our advice is to look past the monthly price tag.

Always verify the exact death benefit dollar amount. Most buyers who default into guaranteed issue would have easily qualified for simplified issue. They miss out on full day-one coverage at a lower cost because they simply never take the time to answer a few health questions.

The Honest Path

Start your search with a simplified issue application. Run your profile through 3 to 5 A-rated carriers via an independent broker. We secure decisions for clients quickly using modern e-applications.

Many carriers now process these applications and issue a decision in just 15 to 30 minutes. If you qualify, lock in the day one coverage at the lower rate immediately. Our team considers guaranteed issue as a necessary fallback option.

It serves a vital purpose for those with severe health histories. It must remain a fallback choice rather than your starting point.

Your Next Steps

We suggest reviewing your current health status before taking action.

- Gather your records: Keep a complete list of your current prescriptions handy.

- Compare multiple quotes: Use an independent broker to find the best rate.

- Verify the details: Ask specifically for a no waiting period burial insurance policy.

Take action today to protect your family’s future.