The Central Question Most Buyers Have

We see many homeowners and business owners struggle to decipher what happens if you die during the graded benefit period. The exact payout amount matters immensely for your estate planning. The beneficiary receives a refund of all premiums paid plus an interest credit for natural causes, or the full benefit for accidental causes.

Our team frequently helps clients evaluate guaranteed issue options when serious health problems arise.

A graded death benefit simply limits the financial risk for the insurer during the first 24 to 36 months of the contract. We view this waiting period as the most critical detail to understand before signing an application. This guide breaks down the specific payout scenarios and explores a practical workaround our team uses to secure immediate coverage.

How Different Causes of Death Trigger Payouts

Insurance companies classify fatalities into two distinct categories during the waiting period. We always verify which structure a specific carrier uses before making a recommendation.

You can rely on these three primary guidelines. Our research shows most policies follow a strict set of rules.

- Death from natural causes during the waiting period: The beneficiary receives a return of all premiums paid, plus interest. Most major US carriers credit about 10% on the total premiums paid, rather than paying the full death benefit. Recent 2024 mortality data from the CDC shows heart disease and cancer cause over 1.3 million US deaths annually. These illnesses make a natural death the most likely scenario.

- Death from accidental causes during the waiting period: The beneficiary receives the full death benefit. The accidental death exception exists in guaranteed issue policies because an accident is not a health-related underwriting risk.

- Any cause after the waiting period: The full death benefit pays out exactly like a standard whole life policy. The coverage remains permanent to help settle property taxes or business debts.

We consider this accident exemption a crucial safety net for active business owners. The CDC reports that unintentional injuries rank as the third leading cause of death in the US, claiming over 197,000 lives in 2024. Families rely heavily on this full payout if a sudden motor vehicle collision occurs.

A Real-Dollar Example

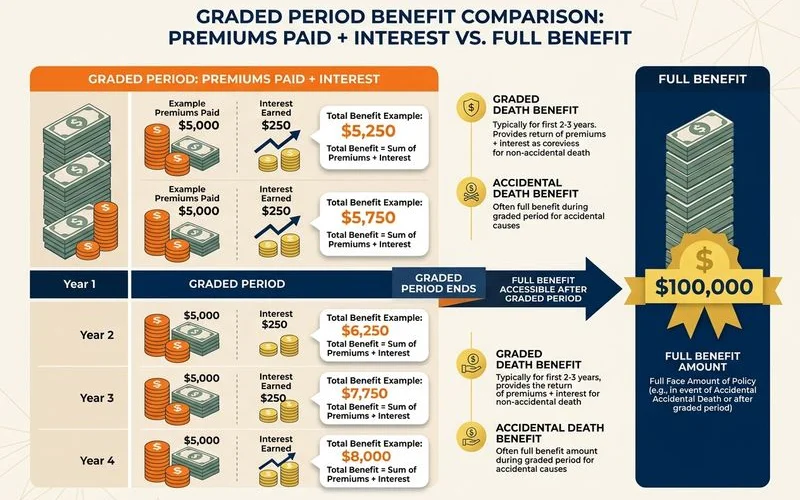

We created this specific calculation to show you the exact financial difference between a natural and an accidental death payout. A $10,000 policy costing $90 monthly pays out exactly $1,386 if the insured dies of natural causes in month 14.

Our goal is to eliminate any confusion about the math behind the return of premiums plus interest. Looking at a concrete scenario makes the contract terms much easier to understand.

The 14-Month Payout Calculation

We regularly use this example for clients planning their estate liquidity. Imagine a 70-year-old commercial property owner applies for a $10,000 guaranteed-issue policy at $90 per month.

We will assume they pass away from a heart attack, which is a natural cause, after exactly 14 months. The math breaks down clearly.

- Total premiums paid: 14 multiplied by $90 equals $1,260.

- Interest credit at 10%: $126 (A standard rate seen with carriers like Gerber Life).

- Total payable to beneficiary: $1,386.

- Comparison: The full death benefit sits at $10,000.

We want to point out what happens if this individual lived past the 24-month waiting period. A natural death in month 30 results in the family receiving the full $10,000 to cover final expenses.

Our analysis also highlights the value of the accident exemption. An auto accident in month 14 forces the carrier to pay the entire $10,000 immediately.

Why This Matters for the Decision

We emphasize this waiting period because it creates a clear financial disadvantage compared to immediate coverage. The graded benefit structure is the primary reason you should always attempt to secure simplified issue coverage first.

Our recommendation is that every applicant should attempt answering a health questionnaire before accepting a guaranteed policy. Avoiding the graded period entirely saves money and provides immediate peace of mind.

The Simplified Issue Advantage

We strongly recommend shopping simplified issue across multiple carriers before defaulting into guaranteed coverage. A 2026 pricing analysis shows a 70-year-old male might pay roughly $74 monthly for a $10,000 simplified issue policy with companies like Mutual of Omaha.

We compare this to the $90 monthly cost of the guaranteed issue policy in the previous example. The simplified option offers several distinct benefits.

- Immediate Coverage: The full death benefit pays out from day one, skipping the graded period entirely.

- Lower Monthly Premiums: Passing a simple health screening lowers the insurer’s risk, which lowers your monthly bill.

- Faster Processing: Applications approve quickly without requiring physical exams or blood work.

Our team frequently sees clients skip the medical questions simply to avoid a perceived hassle. This mistake leaves families with only a small refund instead of the thousands of dollars they expected.

We insist on checking medical eligibility first to secure the best possible outcome for your family. Taking ten minutes to answer a questionnaire protects your assets far better than assuming you need guaranteed issue.

When Guaranteed Issue Is Still Worth It

We consider this product highly valuable when severe health conditions completely disqualify you from other life insurance options. A guaranteed acceptance policy provides essential liquidity for a business owner who cannot pass any medical screening.

Our clients with severe diagnoses rely on these contracts to ensure their families avoid leaving debt behind. The graded period represents a fair tradeoff for guaranteed approval.

Making the Right Strategic Choice

We see guaranteed issue as a perfect fit for specific, severe medical situations. Your health status determines when this product becomes a smart financial move.

- Recent Cancer Treatment: Active or very recent treatments cause automatic declines elsewhere.

- Advanced COPD: Severe respiratory issues typically require guaranteed acceptance.

- Dementia Diagnosis: Cognitive decline disqualifies applicants from simplified issue screening.

Our approach treats the 10% return of premium as a safe holding area for your money. That guaranteed 10% interest often beats standard bank account yields while you wait for the full benefit to activate. The full $10,000 payout then applies for the rest of your life once the 24-month or 36-month wait ends.

We want you to view this permanent coverage as a reliable tool designed for a very specific problem.

Making an informed choice ensures your property and loved ones stay protected. We encourage you to contact a licensed advisor today to compare simplified and guaranteed options in your state.