We talk to adult children every day who want to protect their families from unexpected final expenses. The reality is that setting up coverage for an aging family member requires strict adherence to specific legal guidelines.

Many people ask us if they can get life insurance on a parent without their knowledge.

The simple answer is no, because you must secure their explicit participation to move forward. We are going to explain exactly how consent works and the legal rules you must follow to buy a policy. This guide outlines the legal requirements, the application process, and how to handle situations involving cognitive decline.

The Hard Rule: Parent Must Consent

You absolutely cannot insure a parent without their explicit consent and participation. Every life insurance carrier and state law in the US requires the proposed insured to be actively involved.

We see strict enforcement of this rule across the entire industry to prevent financial exploitation. Insurance fraud is a massive problem, and industry data from 2025 shows that life insurance fraud costs the sector nearly $75 billion annually. The mandatory consent rule acts as the primary defense against these illegal schemes.

The parent being insured must complete several specific steps to proceed. They have to:

- Know about the policy

- Consent to being insured

- Personally answer the health questions on the application

- Sign the application

We frequently receive questions about using a Power of Attorney to bypass this process. A Power of Attorney does not substitute for personal consent on new life insurance applications. Even with full legal authority, you cannot validly answer health questions on behalf of someone else to open a new policy.

What You Can Do With Their Consent

Once your parent agrees to the process, you gain complete control over how you structure the policy. The initial application is usually their only required involvement.

We help families set up agreements where the adult child manages all the ongoing details. You have substantial flexibility to establish clear roles when you buy burial insurance for parents that protect your financial interests.

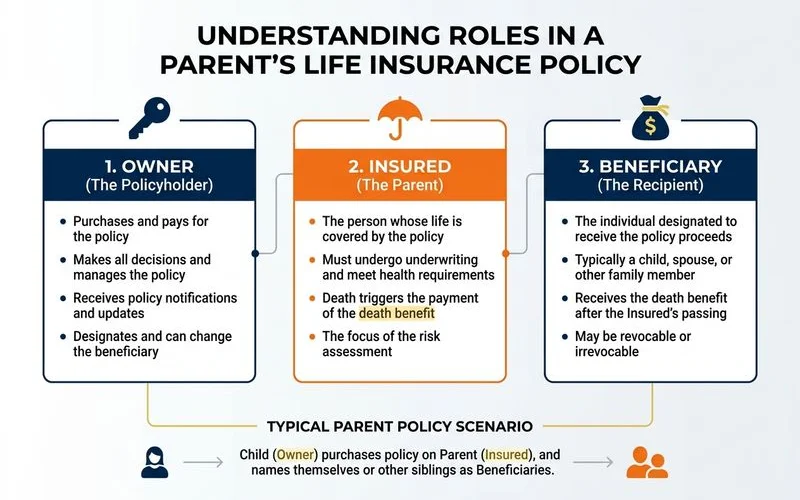

Defining Policy Roles

Setting up the right structure ensures the money goes exactly where you need it. Here is a breakdown of the standard roles you can establish.

| Policy Role | Who Fills It | Responsibilities & Rights |

|---|---|---|

| Insured | Your Parent | Participates in the application and phone interview. No ongoing tasks. |

| Owner | You (The Child) | Controls the policy, changes beneficiaries, and accesses cash value. |

| Premium Payer | You (The Child) | Connects auto-pay to a personal bank account to keep the policy active. |

| Beneficiary | You (The Child) | Receives the death benefit directly, avoiding the probate process. |

We strongly recommend this exact setup for adult children buying coverage for aging parents. This structure allows you to add features like Accelerated Death Benefit riders, which can advance part of the payout if your parent is diagnosed with a terminal illness. Your parent never has to track a bill or manage paperwork.

What Can’t Be Done Without Them

Attempting to bypass your parent during the application process is illegal and constitutes insurance fraud. Carriers will cancel the coverage entirely if they discover unauthorized actions.

We always warn clients about the severe consequences of forging signatures or faking interviews. The insurance company applies a legal principle called “void ab initio” when they uncover application fraud. This Latin term means the contract was completely invalid from the very beginning. The carrier will void the policy, and your designated beneficiary will receive nothing when the time comes.

You must avoid the following illegal actions:

- Filling out the application yourself with their information (without their participation in the phone interview)

- Forging their signature on the application

- Using POA to answer health questions on their behalf

- Buying the policy and “telling them later”

- Buying a policy on someone who lacks legal capacity to consent (advanced dementia, etc.)

We want to make sure your family actually gets the payout they expect. Following the rules ensures the death benefit remains safe and legally binding.

The Phone-Interview Detail

Insurance carriers typically require a short telephone interview to verify identity and health history. This call usually takes 10 to 20 minutes directly with your parent. We know these calls can make older applicants nervous, so you are allowed to sit right next to them to provide moral support.

During the call, the interviewer asks the exact same health questions from the written application. Companies like Mutual of Omaha use this conversation to cross-reference the answers against automated data pulls, such as Milliman IntelliScript prescription histories. The proposed insured must speak in their own voice and confirm their understanding of the contract.

We can help you arrange special accommodations if your parent faces communication challenges. Common accommodations include:

- Professional interpreters for non-English speakers

- In-person signing with a verified notary

- TTY services for the hearing impaired

When a Parent Has Cognitive Decline

Securing a new policy is no longer possible once a parent receives a formal diagnosis of severe cognitive decline. They lose the legal capacity required to sign a binding financial contract.

We see many families struggle when they wait too long to start this process. The Alzheimer’s Association reports that an estimated 7.4 million Americans are living with Alzheimer’s in 2026. This growing health crisis means adult children must plan ahead before memory issues arise. If cognitive decline is already present, carriers will not accept their health answers.

In these specific situations:

- An existing policy can stay in force (you continue paying premiums)

- A new policy generally can’t be placed

- Guaranteed issue is no exception, as it still requires the insured’s consent

We always tell clients that the right time to buy coverage is today. After significant mental decline progresses, your options narrow considerably. Taking action early guarantees you can lock in a policy while your parent can still legally sign.

How to Approach the Conversation

The most effective way to introduce this topic is by framing the policy as a tool to protect you and your siblings from debt. This shifts the focus away from their passing and toward financial practicalities. We recommend opening the discussion with a simple request. You can say, “I want to make sure your funeral and burial costs do not fall on me. Can we put a small policy in place so that is taken care of? I will handle the cost, and I just need 30 minutes for the application.”

Families often underestimate the true expense of final arrangements. The National Funeral Directors Association reports the 2026 median cost of a funeral with a viewing and burial is $8,300. Sharing this specific number often helps parents understand the immediate necessity of coverage. We find that most parents agree readily when the request is framed this way, because it removes the burden from their children.

You can learn more about the exact next steps in the practical how-to guide for securing this coverage.