We frequently see homeowners and business owners carefully protecting their own assets while completely overlooking their aging parents’ final expenses.

If you are currently wondering, should I buy life insurance for my parents, you are addressing a critical financial blind spot. You build wealth and secure properties, yet a sudden $10,000 funeral bill can easily disrupt your carefully managed cash flow.

Our team has watched too many clients scramble to liquidate investments or pull equity just to cover a sudden burial. This financial shock is entirely preventable.

Reviewing the data behind funeral costs reveals why splitting the bill is a flawed strategy. Let’s look at the exact burial insurance for parents options you can use to protect your wealth.

The Two Paths: Should I Buy Life Insurance for My Parents?

When deciding whether to buy a policy for your parents or split the funeral cost later, securing a policy is always the safer financial move for business owners and homeowners. We see families face a harsh reality when a parent has nothing in place. You essentially have two choices.

| Feature | Path A: Small Policy Now | Path B: Wait & Split Later |

|---|---|---|

| Monthly Cost | Modest premium (e.g., $65) | $0 |

| Coverage Timing | In force upon approval | None |

| Family Burden | Zero logistics, death benefit pays costs | High-stress split of a $10,000 to $15,000 bill |

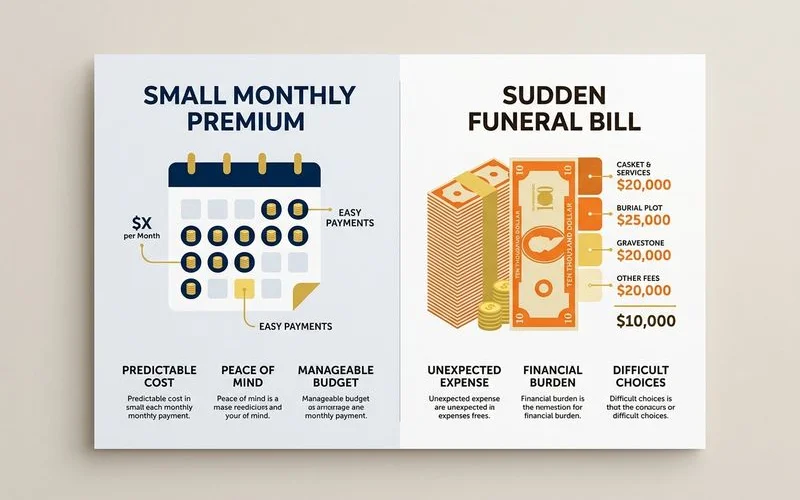

- Path A: Buy a small policy now. A modest monthly premium typically secures $10,000 of coverage. Coverage is in force as soon as the application is approved. The death benefit pays the funeral, burial, and final costs when the time comes.

- Path B: Wait and hope, then split costs later. You pay no monthly cost now. Family members simply split a massive funeral bill later. This typically happens during a high-stress week of grief and family logistics.

Our experience shows these are not equally good options. Path A is significantly cheaper in total. It removes a major source of family friction. Path B leaves real money on the table and places a heavy burden on whoever ends up in charge.

The National Funeral Directors Association (NFDA) reported in 2025 that the national median cost of a funeral with viewing and burial is $8,300. Adding a cemetery plot and headstone easily pushes that well past $10,000. You should buy life insurance for your parents to prevent this sudden drain on your savings.

The Real Math

Looking at the hard numbers proves why a dedicated policy protects your hard-earned equity. We will run the exact figures for a 70-year-old parent in average health in the US.

Path A: $10,000 simplified-issue policy now

- Monthly premium: ~$65 (national average for that profile)

- Paid for 10 years before death: $7,800 total

- Paid for 15 years before death: $11,700 total

- Death benefit paid to family: $10,000 tax-free

- Net family cost over 10 to 15 years: $0 to $1,700

Path B: No policy, pay out of pocket later

- Monthly cost: $0

- Family cost at time of death: $10,000 to $15,000 cash (or more for traditional burial)

- Source: home equity loans, business capital, savings, or credit cards

- Timing: Bill arrives during the week of grief, and logistics happen on a tight timeline

Comparing the total outlay is the advice we always give our clients. Path A is the cheaper choice for most families, even before considering the awkwardness of asking extended family for money. A policy on parent vs funeral cost out of pocket is a clear mathematical win.

The GoFundMe-Among-Siblings Scenario

Relying on a split funeral bill siblings arrangement is the scenario most adult children quietly dread. We understand how quickly a lack of planning turns into a family crisis. When a parent passes without a policy, the funeral home demands immediate payment.

Someone has to step up and act. The conversations that follow usually sound like this:

- “Who can put it on a credit card now and we will reimburse?”

- “How are we going to split this funeral bill among siblings?”

- “Should we do a GoFundMe? Who knows enough people to make it work?”

- “Can we do something cheaper than a traditional service?”

Our research into recent 2026 data shows why crowdfunding is incredibly risky. GoFundMe hosts over 125,000 memorial fundraisers every year in the US, but the average campaign only raises around $2,200 to $2,600.

Nearly a third of these funeral campaigns fail to reach their goal entirely. You cannot afford to risk your personal savings on those odds.

None of these sibling conversations are pleasant. When forced to split a massive bill during a week of grief, families often expose long-standing tensions over money. They happen at the absolute worst time.

A $65 monthly policy bought years earlier easily avoids all of this drama. The policy is emotionally cheaper because no one has to ask anyone for money during a funeral.

What Waiting Costs

Waiting to buy coverage dramatically increases your financial exposure. We advise securing a policy immediately to avoid these three severe consequences:

- Compounding Premium Increases: Life insurance premiums rise by roughly 8% to 10% with each year of the parent’s age.

- Health Reclassification Risks: If health declines, simplified issue coverage may become completely unavailable.

- Graded Benefit Traps: A drop in health forces the parent into a guaranteed issue policy, which requires a strict two to three year waiting period before paying the full amount.

A policy bought at age 70 costs significantly less than the exact same coverage purchased at 75. Our industry data shows that delaying just a few years can nearly double the monthly cost.

Waiting also carries a massive hidden risk. The period between now and “later” is exactly when a sudden tragedy could strike.

We have seen families forced to liquidate business assets because a parent passed away during this waiting period. If the worst happens while you wait, the unplanned $10,000 bill is vastly larger than the planned premium alternative.

How to Start the Conversation

Initiating this discussion with your parents is usually much easier than expected. We recommend treating it like a standard business or estate planning review.

Bringing up documents like an Advance Directive or a living trust provides a natural segue into discussing final expenses. Common framings that work exceptionally well include:

- “I want to make sure your funeral isn’t a financial scramble for me and my siblings. Can we put a small policy in place? I will cover the cost.”

- “I have been organizing my own business and family assets so we are not scrambling later. Can we do 30 minutes on a quote for you?”

- “The cost of a typical funeral in the US now exceeds $10,000. I would rather pay $60 a month than ask siblings to split a $12,000 bill someday. What do you think?”

Our clients find that parents agree readily when the framing emphasizes sparing the family stress rather than dwelling on morbidity. Our walkthrough on how to buy burial insurance for a parent covers the exact next steps once the conversation has happened.

Conclusion

Protecting your family’s savings means making decisions before a crisis hits. We strongly advise securing a policy today rather than leaving things to chance.

If you find yourself wondering, “should I buy life insurance for my parents?”, the data points directly to yes. It is the most logical way to protect your business and home equity from unexpected end-of-life expenses.

Take ten minutes today to review your parents’ current coverage. Reach out to a licensed agent to compare quotes and lock in a manageable rate before prices increase next year.