We often speak with homeowners and business owners looking for a straightforward way to protect their legacy. Paying monthly bills for decades is a hassle that many people prefer to avoid.

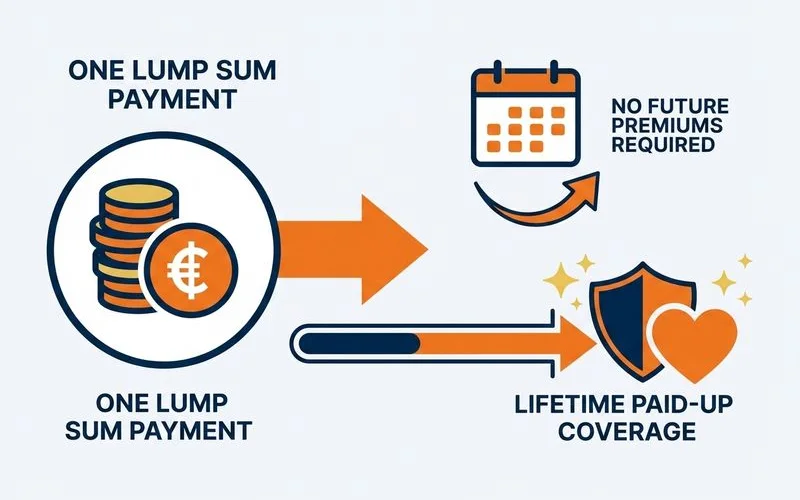

This one-and-done approach turns a single lump sum into permanent protection.

Our team considers single premium whole life insurance to be a strategic alternative to traditional policies.

The following guide breaks down exactly how these one-payment policies work. You will easily learn how to determine if they align with your financial goals.

The Mechanics in Plain Terms

Single premium coverage is exactly what the name suggests. You make one upfront payment to secure a policy that is fully paid for life. No monthly premiums or annual bills will ever arrive in your mailbox.

We see this as a massive advantage for clients who want guaranteed results without ongoing obligations. You simply write one check to put the policy in force. The coverage stays active forever as long as the life insurance carrier remains solvent.

Several factors provide confidence in this long-term stability:

- Major providers like State Farm and MassMutual hold A++ ratings from A.M. Best.

- Highly rated insurers have virtually zero history of solvency failures.

- State guaranty associations offer an additional layer of consumer protection.

The exact premium amount depends on your age, gender, health status, and desired death benefit.

To give you a practical benchmark, consider the typical final expense policy. The National Funeral Directors Association reports the national median cost of a funeral with burial is roughly $8,300 in 2026. This reality makes a $10,000 death benefit a very common starting point for families.

Here is a look at rough estimates for a $10,000 benefit:

| Age & Gender | Health Status | Estimated Single Premium |

|---|---|---|

| 65-year-old Female | Healthy | $5,000 to $6,500 |

| 65-year-old Male | Healthy | $5,500 to $7,000 |

| 75-year-old Female | Healthy | $6,500 to $8,500 |

| 75-year-old Male | Healthy | $7,000 to $9,500 |

Our internal reviews show these numbers are purely illustrative. Actual pricing varies significantly based on the carrier and their specific underwriting guidelines.

The core principle remains consistent across the industry. Your lump-sum payment will generally equal 50% to 80% of the eventual death benefit.

Immediate Paid-Up Status

The defining feature of this product is its immediate paid-up status. The exact moment your premium is received and the policy is issued, your transaction is complete.

Our team appreciates the simplicity of this structure for busy business owners. This setup is fundamentally different from a paid-up addition rider on a standard term policy. The entire contract is fully funded from day one.

You immediately gain several powerful guarantees:

- Full death benefit in force right away (assuming simplified issue underwriting).

- Complete elimination of all future premium obligations.

- Immediate cash value generation.

- Lifetime coverage backed by the solvency of the carrier.

Simplified issue underwriting means you can often secure this coverage without a comprehensive medical exam. The application process typically involves a basic health questionnaire and a prescription history check. Approval can sometimes happen within a few days.

Cash Value and Tax Treatment

Single premium contracts build cash value much differently than traditional monthly-pay policies. The insurance company receives your entire deposit upfront and begins applying interest immediately. This means your cash value starts at a substantial percentage of the premium paid and grows steadily over time.

We must highlight a critical tax rule that applies to these specific policies. Under the Technical and Miscellaneous Revenue Act of 1988, these contracts are classified as Modified Endowment Contracts (MECs). This classification happens because a single premium payment automatically fails the IRS 7-pay test.

The 7-pay test limits how much cash you can deposit into a life insurance policy within the first seven years. Exceeding this limit triggers the MEC status permanently.

MEC classification introduces specific tax consequences:

- The death benefit remains completely tax-free to your beneficiaries.

- Cash value withdrawals or loans during your lifetime are taxed on a last-in, first-out basis.

- Any growth or gains withdrawn are taxed as ordinary income.

- Withdrawing funds before age 59½ triggers an additional 10% IRS penalty.

For final expense planning, this MEC status is rarely a problem. The policy is intended to pay out at death rather than serve as a liquid savings account.

The income tax-free nature of the death benefit remains perfectly intact. You simply need to understand these rules before assuming the cash value can act as an emergency fund.

When This Product Fits

This strategy is highly effective when you have idle cash and a specific legacy goal.

We frequently help clients transition funds from matured CDs or recent inheritances into these guaranteed contracts. The minimum required premium often starts between $10,000 and $50,000 depending on the provider.

A single premium policy is typically a great fit if:

- You want to convert a lump sum of cash into a larger guaranteed benefit for your family.

- You are an adult child buying coverage for a parent and want a one-and-done transaction.

- You absolutely refuse to deal with the hassle of monthly premium bills.

- You are estate planning and want to pass a specific tax-free amount outside of probate.

Locking up a large amount of capital is not the right move for everyone.

Our advisors always verify that clients have sufficient liquid emergency funds before making this recommendation.

Monthly-pay policies are generally better when:

- You do not have a substantial lump sum readily available.

- You prefer to keep your cash highly liquid and accessible for business opportunities.

- You want to use the cash value as a tax-advantaged savings vehicle without MEC penalties.

For a detailed cost comparison and a deeper look at your options, see our guide on single premium vs monthly-pay.