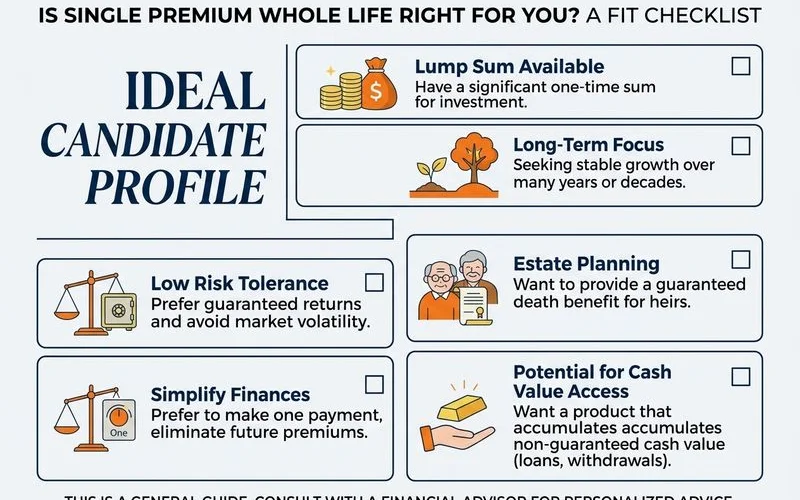

The Right Fit Profile

Single premium whole life isn’t the right product for everyone. It works best for buyers who match one or more of the following profiles:

1. Senior with cash on hand. You have savings, a CD maturing, or an inheritance you want to deploy toward end-of-life coverage. Converting a portion of those funds into a paid-up policy guarantees the funeral and final costs are covered without leaving family scrambling later.

2. Adult child buying for a parent. You’ve decided to put coverage on mom or dad. You don’t want to deal with monthly premium bills from an aging parent’s account or coordinate with siblings on splitting monthly costs. Single premium pays once and ends the administrative work.

3. Set-it-and-forget-it preference. Some buyers simply prefer not to have recurring premium obligations in retirement. Single premium delivers permanent coverage with no future bills to manage.

4. Estate planning use. For larger estate plans where someone wants a specific tax-free amount outside the probate process, single premium can serve as a discrete bequest tool.

When Monthly-Pay Is Smarter

Single premium isn’t always the right answer, and our single premium vs monthly-pay comparison runs the full numbers. Monthly-pay whole life is usually better when:

- You don’t have the lump sum readily available. Monthly-pay spreads the cost.

- You’d rather keep your cash liquid and accessible. Once a single premium is paid, that money is tied up in the policy (with cash-value access available but subject to taxation).

- You’re earlier in life (under 70) and have decades of expected premium payments. The total cost paid via monthly premiums over 20+ years often exceeds the single premium, but the cash flow management is easier.

- You’re using insurance as part of a broader savings strategy where MEC classification (which applies to single premium policies) would be a problem.

The Adult-Children-Buying-for-Parents Scenario

This is one of the most common scenarios for single premium in final expense. The pattern looks like:

- Mom or dad has nothing in place. Adult children realize this and want to address it.

- Siblings discuss splitting the cost of a funeral that’s likely coming.

- They decide to put a policy on the parent now to avoid splitting a $10,000–$15,000 bill later.

- Single premium appeals because it ends the conversation — no monthly bill to track, no ongoing premium discussion among siblings.

Buying a policy on a parent requires the parent’s consent and participation in the application. Single premium can be funded from one sibling’s account or contributed jointly. The key point: once paid, the policy is permanent and the administrative burden is over.

Liquidity Considerations

The biggest argument against single premium is liquidity. Once you pay the lump sum, that money is in the policy. You can borrow against the cash value or withdraw a portion, but those moves have tax implications (because single premium policies are typically classified as MECs).

If you might need the cash for other purposes — medical care, a major expense, helping out children or grandchildren — keeping it liquid in a high-yield savings account or CD may be smarter than committing it to a single premium policy. The death benefit is valuable, but it’s not accessible to you while you’re alive in the way liquid savings are.

How to Decide

Ask yourself three questions:

- Do I have the lump sum without straining my liquidity?

- Would I rather pay once and never see a premium bill again?

- Is my goal genuinely to deliver a benefit at death, not to use this as a savings tool?

If you answered yes to all three, single premium fits. If you hesitated on any, monthly-pay simplified-issue whole life is probably the better fit — same product mechanically, different payment schedule.