The Core Tradeoff

Single premium whole life and monthly-pay whole life ultimately deliver the same thing — a tax-free death benefit to your beneficiary — but they differ on cash flow, total cost, and flexibility. Here’s how they compare for the same buyer profile.

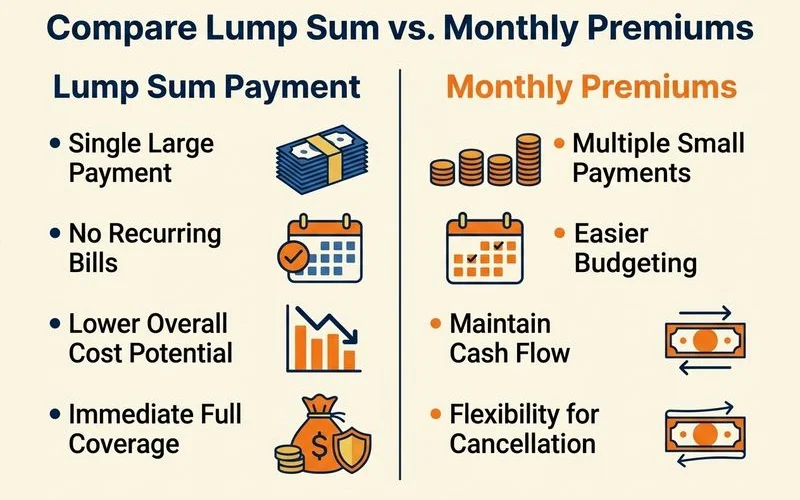

Single premium: One large payment upfront, no future obligations, slightly lower total cost over the policy’s life. Requires liquidity.

Monthly-pay: Smaller recurring payments for life (or for a set period with limited-pay variants), higher total cost over many years, easier on cash flow.

Same-Policy Cost Comparison

For a 65-year-old healthy female buying a $10,000 final expense policy:

| Approach | Single Premium | Monthly-Pay |

|---|---|---|

| Upfront cost | ~$5,500 | $0 (first premium ~$50) |

| Monthly cost thereafter | $0 | ~$50/month |

| Total cost after 20 years | $5,500 | ~$12,000 |

| Coverage in force | $10,000 | $10,000 |

| Cash-flow burden | High upfront, none after | Modest, ongoing |

So over 20 years, single premium costs about half what monthly-pay does in total dollars. But single premium requires the buyer (or someone funding on their behalf) to have $5,500 available now.

For a 70-year-old male, the comparison shifts a bit:

| Approach | Single Premium | Monthly-Pay |

|---|---|---|

| Upfront cost | ~$7,000 | $0 (first premium ~$80) |

| Monthly cost thereafter | $0 | ~$80/month |

| Total cost after 15 years | $7,000 | ~$14,400 |

The longer you expect to live (and pay monthly premiums), the larger the single-premium savings — but the larger the upfront commitment.

Cash-Flow Tradeoffs

Single premium pros:

- One-time transaction, never see another bill

- Lower total dollar cost over the policy’s life

- No risk of lapse from missed payments

- Easier for adult children to fund without ongoing coordination

Single premium cons:

- Substantial upfront commitment

- Cash is tied up in the policy (cash-value access has tax implications due to MEC classification)

- If you need liquidity for other purposes later, you can’t easily reverse

Monthly-pay pros:

- Manageable monthly cost, fits typical retiree budgets

- Cash stays liquid in your accounts

- Easy to start without a large upfront sum

- More flexible if your situation changes

Monthly-pay cons:

- Premium bills for the rest of your life

- Higher total dollar cost over time

- Risk of lapse if a payment is missed (most policies have a grace period but not unlimited)

- Annual reminders of the topic for buyers who’d rather not think about it

The “Set It and Forget It” Appeal

For some buyers, the entire appeal of single premium is psychological. They don’t want to manage another monthly bill. They don’t want their adult children to be coordinating premium payments later. They want the coverage in place, paid, and done.

This is genuinely a valid preference. If avoiding ongoing administration is worth a few hundred dollars of upfront cost difference, single premium makes sense. The product solves a real problem for buyers who prioritize simplicity over cash-flow optimization.

Who Each Suits

- Single premium: Buyers with cash on hand, those buying for a parent, estate planners wanting a discrete tax-free bequest, retirees who’d rather not deal with recurring bills.

- Monthly-pay: Buyers without lump-sum availability, those who’d rather keep their savings liquid, anyone who wants flexibility to surrender or change coverage later without large reversed transactions.

For most working-class and middle-class buyers without significant savings, monthly-pay is the realistic answer. Single premium fits a narrower profile but solves a real problem for that profile — our guide on who single premium whole life is right for maps out exactly which buyers benefit most.