The Self-Check

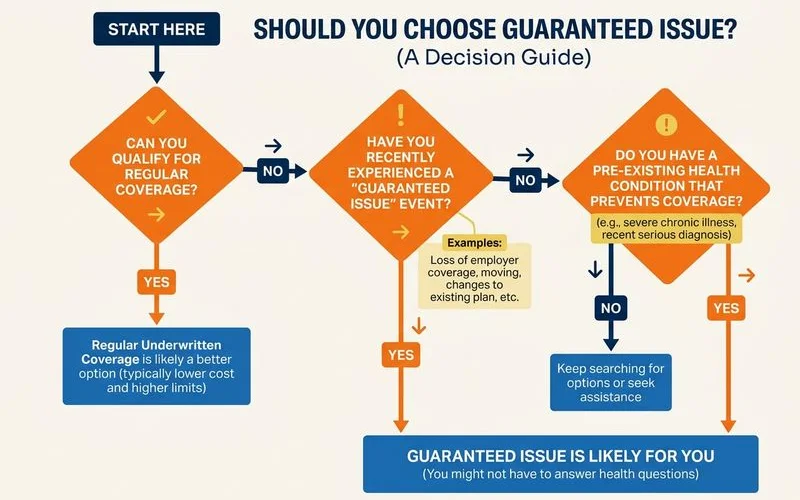

Guaranteed issue is built for people whose health truly disqualifies them from simplified-issue underwriting at any carrier. That’s a smaller group than most buyers assume. Run through this self-check before defaulting in.

You probably do need guaranteed issue if:

- You are in active treatment for cancer, or were diagnosed within the last 12–24 months

- You have advanced COPD requiring continuous oxygen

- You have been diagnosed with dementia or Alzheimer’s

- You had a severe stroke or heart attack within the past 12 months

- You are on dialysis for kidney failure

- You have a recent organ transplant (within the lookback window)

- You have HIV/AIDS in some states (varies by carrier)

You probably do not need guaranteed issue if:

- You have well-controlled Type 2 diabetes (even on insulin for some carriers)

- You have controlled high blood pressure

- You have a cancer history that’s 5+ years out from treatment

- You had a heart attack 5+ years ago and have been stable since

- You’re managing common conditions with medications, no recent hospitalizations

The Cost Penalty of Defaulting In

Guaranteed-issue premiums typically run 30–60% higher than simplified-issue for the same coverage and applicant. On a $10,000 policy held for 15 years, that’s $3,000–$6,000 more out of pocket — plus the 2- to 3-year waiting period during which only premiums-plus-interest pay out on natural-cause deaths.

If you can qualify for simplified issue and end up with guaranteed issue anyway because no one asked, you’ve made an avoidable mistake. The decision is reversible while you’re shopping, but not after you’ve placed the policy.

What an Honest Process Looks Like

A good independent broker will:

- Run your situation through 3–5 A-rated simplified-issue carriers.

- Report back which (if any) would approve you and at what tier.

- Only recommend guaranteed issue if simplified issue isn’t realistic.

- Explain the graded benefit period clearly before placement.

A bad process: someone steers you straight to guaranteed issue without shopping simplified first. If that’s happening, the agent is captive (only sells one carrier’s guaranteed-issue product) or working on the wrong incentives. Step away.

Bottom Line

Guaranteed issue is genuinely valuable for the people who need it. It also costs significantly more than necessary for the people who didn’t. The honest path is shopping simplified issue first, across multiple A-rated carriers — and falling back to guaranteed only when it’s the real answer for your situation.