We know how frustrating it is to quote a policy and see the rate climb because of a few missed birthdays. Homeowners often want to protect their property from being sold to pay for final expenses. A 2026 industry review shows that the national median cost of a funeral with viewing and burial hovers around $8,300, making burial insurance cost by age a critical factor in planning.

As a professional service team, we see directly how quickly medical bills and probate fees push that number well over $10,000. These rising costs leave grieving families scrambling for cash, which is exactly why burial insurance exists in the first place.

Let us look at the actual data behind pricing and explore practical ways to lock in the lowest possible premium.

Age Drives the Premium More Than Almost Anything

Age is the single largest factor in determining your final expense rate by age. We track pricing trends across major carriers, and the data clearly shows that every birthday increases your cost. Other than tobacco use, carriers price your exact age into their rate tables at the time of application.

The climb steepens significantly after age 70. A $10,000 policy at 60 is meaningfully cheaper than the exact same policy at 75. This holds true even for the same person in the exact same health.

A recent 2026 data analysis reveals exactly how much waiting costs you, highlighting these core facts about age-based pricing jumps:

- The Annual Penalty: Waiting a single year typically adds 8% to 12% to your premium.

- The Age 75 Cliff: The sharpest rate jump occurs between ages 75 and 80.

- The Percentage Spike: A woman’s average monthly rate climbs by 44% during that five-year window, while a man’s rate jumps 45%.

- The Lifetime Lock: Final expense is a whole life product, meaning a rate locked in at 60 remains identical at age 90.

Our agents will always give you an honest recommendation to buy coverage sooner rather than later. The premium you lock in today is the exact premium you keep for life.

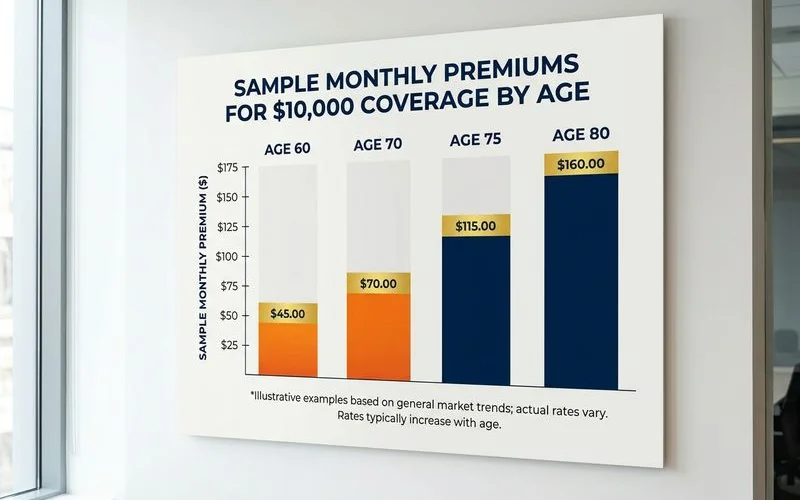

Sample Monthly Premiums (Illustrative)

These bands give you a realistic look at $10,000 of simplified-issue whole life coverage for non-tobacco users with manageable health. We pulled these illustrative figures to show standard market pricing across major carriers. Actual rates vary by carrier, gender, and your specific underwriting class.

| Age | Female | Male |

|---|---|---|

| 60 | $40 to $55 | $50 to $70 |

| 70 | $60 to $85 | $75 to $105 |

| 75 | $85 to $120 | $105 to $150 |

| 80 | $120 to $170 | $145 to $210 |

Our team recommends checking specific companies like Transamerica or Mutual of Omaha for the most competitive rates in your 50s and 60s. Understanding your specific burial insurance cost for a 75 year old or a 60 year old helps you budget correctly. Tobacco users add 30% to 50% to each of these bands.

Guaranteed-issue policies with no health questions run 30% to 60% higher than simplified-issue at every age. These guaranteed plans also include a two-year or three-year graded benefit period. See how cost works for the underlying mechanics.

The Smoker Effect

Tobacco use triggers a massive premium surcharge that can cost you thousands of dollars over the life of your policy. We see a 65-year-old non-tobacco female paying around $55 per month for a $10,000 benefit. The same applicant flagged as a tobacco user pays closer to $80 or $90.

Over 20 years, that tobacco surcharge alone easily runs $6,000 or more on a modest policy. This extra expense cuts directly into the funds your family could use to settle business debts or mortgage payments.

Our experience shows that carriers classify almost all nicotine products as tobacco use. Vaping, chewing tobacco, and nicotine patches will trigger the smoker rate just like cigarettes.

Most carriers require 12 consecutive months completely smoke-free to reclassify you to a non-tobacco rate. A handful of strict companies require 24 months. If you have successfully quit, ask the agent during the application because this is one of the single biggest controllable levers on your premium.

Here are a few insider facts about tobacco classifications:

- The Cotinine Test: Some carriers allow occasional cigar use, defined as fewer than 12 a year, at non-smoker rates if you pass a cotinine test.

- The Penalty Size: The standard surcharge is 30% to 50% higher than the baseline rate.

- The Carrier Difference: Companies like Americo sometimes require 24 months tobacco-free, making carrier selection critical.

- The Reclassification: You can often apply for a rate reduction after hitting your 12-month tobacco-free milestone.

Why Locking In Younger Is Cheaper

Whole life premiums never increase after the issue date, but insurers calculate your rate based entirely on your exact age at application. We want business owners to realize that waiting leaves your family exposed to unnecessary financial risk. Waiting one year typically adds roughly 2% to 4% to the base premium in your earlier years, but that penalty accelerates.

Waiting five years can add 20% to 25% to your monthly cost. Waiting ten years can easily double it.

Our data confirms that inflation and health changes make waiting dangerous:

- The Inflation Factor: Funeral costs experience an average inflation rate of over 3.5% per year.

- The Moving Target: A service that costs $8,300 today will cost significantly more by the time your family actually needs it.

- The Health Wildcard: A sudden prescription change next year could disqualify you from standard rates.

If you know you want coverage and your health is stable, waiting never saves money. The opposite is completely true. Every single year you wait, the locked-in rate gets permanently higher.

Bridge to a Real Quote

A national price band is useful for a quick sanity check, but only an actual quote from an A-rated carrier tells you your true cost. We highly recommend using an independent broker who can search across multiple carriers instead of just one. A free, no-obligation quote takes about two minutes.

This process produces a real comparison based on your specific health and age instead of a generic sales pitch.

Our agency always checks a carrier’s National Association of Insurance Commissioners (NAIC) complaint index before recommending them. A score below 1.00 indicates fewer complaints than average, which means a smoother payout process for your grieving family.

Take action today to protect your home and business assets.

Compare your options, review your specific burial insurance cost by age, lock in your exact health class, and secure the lowest possible premium for life.