Business owners and homeowners often assume their physical assets will automatically cover their end-of-life expenses.

We see this misconception lead to serious financial stress. Probate processes can lock down property and bank accounts for months. Your family still has to pay the funeral home right away.

The primary question then becomes, how much does final expense insurance cost to prevent this liquidity crisis?

Let’s look at the current 2026 data, what it actually means for your bottom line, and explore a few practical ways to protect your estate.

The Honest National Range

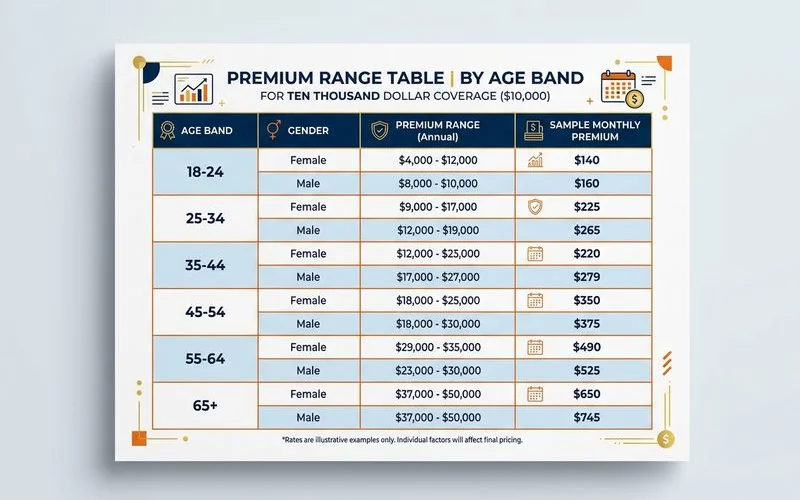

For most people aged 50 to 75, a final expense coverage amount of $10,000 runs roughly $50 to $100 per month. We use this realistic baseline because it aligns with current funeral expenses. According to the National Funeral Directors Association in 2026, the median cost of a funeral with viewing and burial is over $8,300.

Our team finds that your actual number could land anywhere inside or outside that band. A 52-year-old non-smoking woman buying $10,000 in coverage might pay in the $30s monthly.

We see that a 78-year-old man with controlled diabetes might pay in the $110s for the exact same coverage. Both examples are completely normal. These variables explain why a generic quote off a billboard tells you almost nothing about your own price.

What Actually Moves the Premium

Age, gender, tobacco use, and overall health are the four major variables that drive your premium differences. We always evaluate these factors first because they dictate your exact monthly payment.

Age

Premiums rise with each birthday you celebrate.

We remind clients that locking in a policy at age 62 saves a meaningful amount of money compared to locking in at age 72. Check out the cost-by-age guide for sample numbers at 60, 70, 75, and 80.

Gender

Women generally pay less than men at every single age tier.

Our data shows this is because of longer average life expectancies. This pricing trend remains consistent across virtually every major insurance carrier.

Tobacco Use

Cigarette use is the single biggest controllable factor in your pricing.

We see tobacco-rate premiums often run 30% to 50% higher than standard non-tobacco rates. Ask your agent about reclassification if you use:

- Cigarettes or cigars

- Chewing tobacco

- Nicotine patches or gum

- Vaping products

Most carriers require 12 months smoke-free to lower your rate.

Health Conditions

A health condition that earns a standard-rate approval at one carrier may trigger a decline at another.

We consider this underwriting gap the main reason why shopping multiple carriers is incredibly valuable for business owners. For example, a person with controlled Type 2 diabetes might get excellent final expense rates from Mutual of Omaha but face higher premiums elsewhere.

The Carrier-Spread Problem

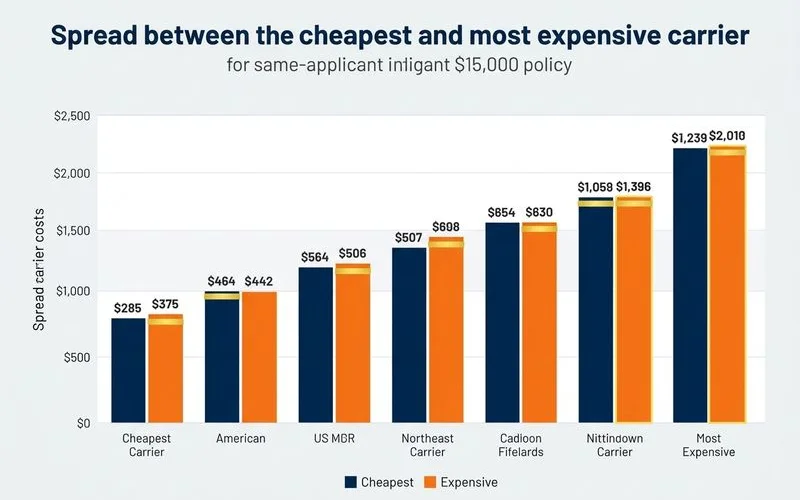

Most quote sites refuse to show you the full market picture.

We want you to know that on a $15,000 policy, the spread between the cheapest and most expensive carrier for the exact same person can be $30 to $50 per month. This translates to $360 to $600 per year in wasted money on identical coverage. Over 10 years, that price difference adds up to thousands of dollars.

Our experts view that massive gap as the strongest argument against buying from a captive agent.

A captive Colonial Penn agent only sells Colonial Penn products. A captive Lincoln Heritage agent only sells Lincoln Heritage coverage. They get one carrier’s underwriting rules and one specific price point.

We prefer the independent agent route because it accesses dozens of carriers to find the best fit.

Sample Numbers (Illustrative Only)

These figures represent a general burial insurance cost for standard applicants.

| Profile | Coverage | Typical Monthly |

|---|---|---|

| Female, age 55, non-smoker, healthy | $10,000 | $35 to $50 |

| Male, age 65, non-smoker, controlled diabetes | $10,000 | $65 to $95 |

| Female, age 72, non-smoker, mild COPD | $15,000 | $110 to $160 |

| Male, age 78, non-smoker, heart attack 5+ years ago | $10,000 | $120 to $180 |

These are illustrative bands for simplified issue policies.

We typically see guaranteed issue plans run much higher. These specialized policies cost 30% to 60% more for the exact same coverage.

Understanding the Waiting Period

Guaranteed issue policies also add a strict two-year or three-year graded benefit period.

We urge you to understand this crucial US regulation before buying. If you pass away from natural causes during those first two years, the carrier will not pay the full death benefit. They will typically refund your paid premiums plus an extra 10% interest instead.

The takeaway: National price ranges are useful as a sanity check, not as a guaranteed quote. Your real monthly premium burial cost depends entirely on which carrier you apply with. We find that the right carrier for your specific profile is rarely obvious from the outside looking in.

Why a Billboard Quote Tells You Nothing

Mass-market quotes from TV ads, billboards, and junk mail usually advertise the absolute lowest possible number. They highlight the rate for a healthy 50-year-old non-smoking woman applying for the smallest coverage tier available.

We know that almost nobody actually qualifies for those teaser rates. Watch out for these common mass-market marketing tricks:

- Per-unit pricing: Advertising a low $9.95 rate that only buys a tiny fraction of the coverage you actually need.

- Age lockdowns: Quoting rates for a 50-year-old when the average applicant is 65 or older.

- Stripped-down policies: Selling accidental-death-only plans disguised as full final expense coverage.

By the time their underwriting department adjusts for your actual age, health, and gender, the real number can be twice or triple the advertised rate.

We admit that practice is not necessarily dishonest, but it is certainly not useful for a serious homeowner planning their estate. A free, no-obligation quote through an independent agent is the only reliable path forward.

We provide a practical way to find your actual rate across multiple A-rated carriers like Transamerica or Aetna. You can finally get real numbers without sitting through a high-pressure sales pitch first. Reach out today to compare your options and secure your family’s financial future.