What the Mailer Is

You’ve probably seen one. An official-looking postcard, often with a state seal or eagle, addressed to seniors. The headline reads something like “State-Regulated Burial Program — Final Notice” or “Senior Burial Benefit Reserved for [Your State].” A return-address box, a phone number, a deadline.

It looks like a government notice. It isn’t. There is no “state-regulated burial program.” The mailer is marketing material from an insurance company or a lead-generation firm. The “regulated” language refers to the fact that all insurance is regulated by state insurance departments — which is true of every policy ever sold. It’s not a special program.

Why It Works

These mailers work because they prey on two things: trust in government communications and anxiety about end-of-life planning. The official-looking design suggests authority. The “final notice” or “limited time” language creates pressure. Many recipients respond before realizing they’re being sold a product.

What you typically get for responding:

- A phone call from an agent (or a series of agents) who’s bought your information from the mailing firm.

- A pitch for a guaranteed-issue policy at a single carrier’s rate — usually one of the most expensive coverage types available.

- Follow-up calls and mailers for weeks or months afterward.

You don’t get a special government rate. You don’t get a benefit other seniors can’t access. You get the same burial insurance product available everywhere, sold to you by a salesperson on commission.

The Tactics, Plainly

- Official-looking design — government seals, eagles, formal envelopes, reference numbers that look like case files.

- Urgency language — “final notice,” “respond by [date],” “limited reservation.”

- Vague “program” language — “state-regulated,” “senior benefit reserved,” “burial program” — none of which describe actual policy mechanics.

- Phone-only response — usually no website to research, just a phone number that routes to a sales agent.

None of this is illegal. But it’s misleading enough that several state insurance departments have issued public warnings about it.

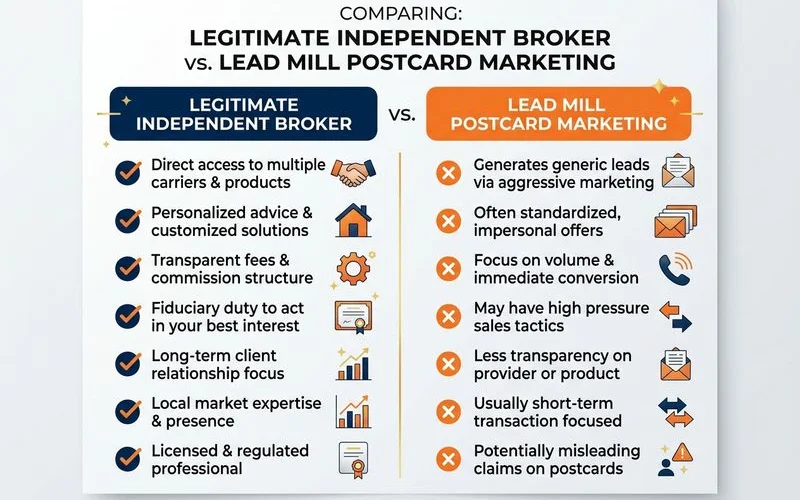

How to Tell a Legitimate Broker

A legitimate independent broker:

- Has a working website with named principals and real contact information.

- Discloses how they get paid (referral fees, agent commissions).

- Can shop multiple A-rated carriers, not push one company.

- Provides educational content before the sales conversation.

- Doesn’t use “final notice” or “state-regulated” framing.

The simplest sanity check: look up the agency on your state’s Department of Insurance website. Licensed agents and brokers must be searchable there. If you can’t find them, that’s the answer.

What to Do If You Already Responded

You haven’t committed to anything. You can still:

- Stop answering follow-up calls. Once on the call list, you may get them for months — your state’s Do Not Call registry can help.

- Shop your situation with an independent broker who can compare multiple A-rated carriers. Whatever the mailer-agent quoted, an independent agent can usually beat it.

- If the agent is being aggressive, you can report them to your state Department of Insurance.

The product itself — final expense whole life insurance — is legitimate and worth having. It’s just that the mailer is one of the worst ways to buy it. A free, no-obligation quote from a reputable independent broker will almost always get you better coverage at a better rate.