The Big Picture

We often see homeowners and business owners worry that a medical diagnosis will block them from protecting their families. That concern is incredibly common when applying for hard-to-place burial insurance.

An $8,300 median funeral bill can force your loved ones to dip into business capital or home equity.

Our recent 2026 data shows that finding affordable burial insurance for diabetics is entirely possible. Most people with this condition qualify for a simplified issue policy at standard rates.

The secret lies entirely in which carrier you select.

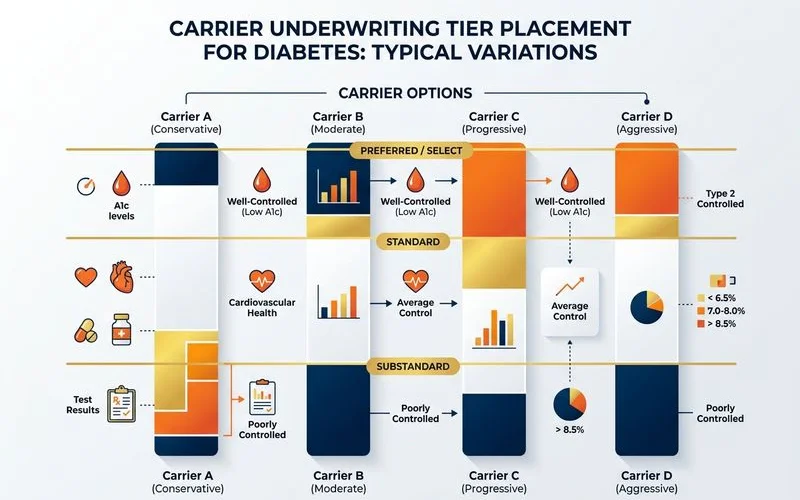

We have personally seen how underwriting standards vary wildly across A-rated carriers. A 68-year-old applicant with Type 2 diabetes taking metformin might get preferred rates at one company.

That exact same person could get graded coverage at another.

How Carriers Look at Diabetes

Our underwriters match applicants to carriers based on specific A1C levels, medication types, and diagnosis age. Your exact medical details determine if an insurer will offer standard life insurance diabetes rates. Protecting your commercial property or family estate requires securing the best possible premium.

We look closely at these key underwriting factors during our review process:

- Type 1 vs Type 2: Carriers treat Type 2 much more leniently. Options exist for Type 1, but the pool of specialized companies is smaller.

- Medication history: A prescription for Metformin is usually viewed favorably. A daily insulin requirement triggers strict handling at some companies, but carriers like Mutual of Omaha often accept it without penalties.

- A1C score: An A1C under 7.0 is the gold standard for preferred rates in 2026. Scores between 7.1 and 8.5 usually secure standard approval, while anything above 9.0 pushes you into higher risk categories.

- Age of onset: A late-in-life diagnosis is much easier to underwrite than a childhood diagnosis.

- Secondary complications: Issues like neuropathy, retinopathy, or recent amputations limit you to guaranteed acceptance plans.

- Combined risks: Adding heart disease or COPD to a diabetes diagnosis complicates your approval odds significantly. If a cardiac condition is also in play, our guide to Final Expense Insurance With Heart Disease covers how carriers stack those risks.

These details dictate your final premium cost. Knowing your exact numbers prevents surprises and helps preserve your business assets.

Our team highly recommends pulling your latest lab results before starting an application. A quick review of your medical chart streamlines the entire process. This proactive step keeps your application moving quickly.

What Tends to Approve Where

We typically see controlled Type 2 diabetes secure standard coverage from day one. Finding insulin dependent burial coverage at standard rates requires applying to very specific carriers. This choice dictates whether your policy pays out immediately or imposes a two-year waiting period.

Our agents analyzed 2026 pricing data to reveal clear patterns for approval. A 65-year-old non-smoker with well-managed diabetes can expect premiums around $35 to $60 per month. Here is a breakdown of common health profiles and their expected outcomes:

| Health Profile | Typical Underwriting Outcome | Carrier Examples |

|---|---|---|

| Type 2, oral meds only, A1C < 7.5 | Preferred or standard at most carriers | Mutual of Omaha, Transamerica |

| Type 2, on insulin, A1C 7.1-8.5, no complications | Standard at many, graded at strict carriers | AIG, Aflac |

| Type 2, insulin, A1C > 9.0 | Graded or guaranteed issue | Various specialized carriers |

| Type 1, controlled, no complications | Standard at specialized carriers, graded at most | Mutual of Omaha |

| Any type + major complications | Graded or guaranteed issue | Guaranteed acceptance providers |

We share these figures to set realistic expectations based on recent industry standards. The right carrier for your specific situation depends on your full health profile. Working with an independent agent who handles these cases daily will point you toward the most favorable companies.

What to Have Ready When You Apply

Our process requires a complete list of your medications and recent lab results. Preparing your medical history in advance speeds up your approval time. This organization ensures your business partners or family members get coverage in place quickly.

We use this information to match you with the most forgiving insurance provider. Carriers actively verify your answers using third-party systems. You must gather the following specific details before applying:

- Current medications, exact dosages, and pharmacy records

- Most recent A1C reading from within the past twelve months

- Official diagnosis date and specific diabetes type

- Documented complications and their current stage

- Recent hospitalizations or emergency room visits

Our agents always remind clients that insurance companies check the Medical Information Bureau database. This system shares application history among more than 500 member carriers. Providers also pull your prescription history through tools like Milliman IntelliScript.

We advise you to answer every health question with absolute honesty. Discrepancies between your answers and these databases can trigger immediate declines. Accurate reporting prevents claim disputes later and keeps your family estate protected.

The Soft Bridge

Our team knows that a diabetes diagnosis does not automatically force you into guaranteed issue plans. Most homeowners and business owners with manageable symptoms qualify for simplified issue policies.

Choosing the right A-rated carrier makes the difference between a waiting period and day-one protection.

We strongly encourage getting a real quote comparison before assuming the worst. This choice prevents your family from absorbing unexpected funeral costs.

You deserve a policy that properly covers your estate without draining business assets.

Our specialists are ready to help you find the perfect fit. Reach out today to review your exact options.

Secure the affordable coverage you need right now.