Our team fields questions every week from property owners about securing life insurance after a heart attack. Many people assume a recent cardiac event automatically disqualifies them from affordable coverage.

The reality is that underwriters evaluate your specific medical timeline rather than a single diagnosis.

We will break down exactly how insurance carriers view your history. This guide covers real costs and the specific companies offering the best approval odds. Knowing these details helps you secure the protection your family needs.

Time Since the Event Is Everything

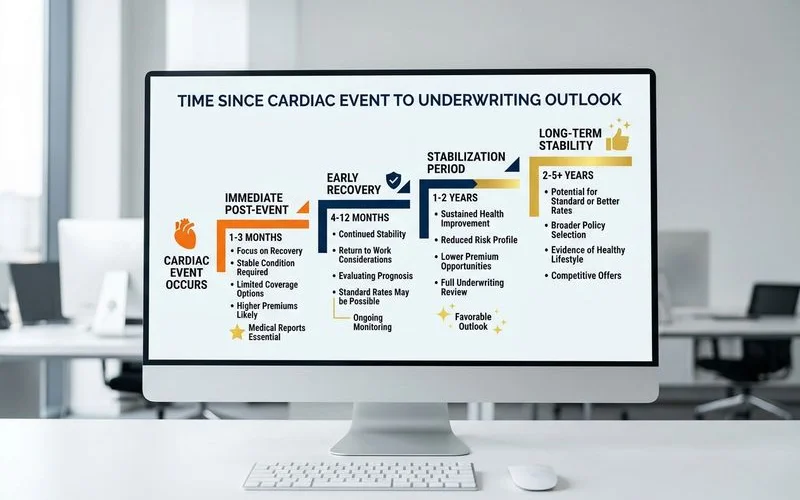

Our underwriting experience shows that timing dictates your approval odds more than any other factor. Insurance carriers look closely at how many months have passed since your cardiac event. A 2026 mortality study indicates that roughly one in three deaths in the US relates to cardiovascular disease.

We know this statistic makes companies cautious during the first year of recovery. The further past the event you get, the better your chances of securing standard simplified-issue rates.

- Within 12 months of heart attack or major procedure: Guaranteed issue is the realistic path.

- 12 months to 2 years post-event, stable: Graded simplified issue at some carriers.

- 2 to 5 years post-event, stable: Standard simplified issue at multiple carriers.

- 5 or more years post-event, stable: Treated like any other standard applicant.

Our agents find that waiting until your two-year anniversary often provides access to cheaper day-one coverage. Many carriers will offer their best preferred rates once you hit the five-year mark. Getting standard approval means your cardiac history is noted but not heavily penalized.

What Counts as “Stable”

Our clients often wonder how an insurance company defines medical stability. Underwriters require concrete proof that your heart function is holding steady. They check recent EKG and echocardiogram results to confirm your recovery.

We typically look for five key indicators before submitting an application.

- No additional cardiac events since the last one.

- No recent ER visits for chest pain or arrhythmia.

- Medication regimen unchanged for at least six months.

- Recent stress test or cardiologist follow-up with reassuring results.

- Reasonable management of related conditions, specifically high cholesterol, hypertension, or Type 2 diabetes.

Any recent escalation resets the stability clock at most carriers. New symptoms, medication changes, or hospitalizations signal a higher risk profile.

Our advice is to plan your application when your clinical picture has been steady for a full year. This patient approach prevents unnecessary declines on your insurance record. A clean recent history makes finding a great rate much easier.

Stents, Bypass, and Procedures

We treat stent placement and bypass procedures as major cardiac events during the quoting process. Timeframes for these surgeries follow the exact same pattern as a standard heart attack. Underwriting guidelines evaluate the total time elapsed since the actual procedure date.

Our team sees a distinct timeline for surgical approvals.

- Under 1 year: Guaranteed issue is usually the only option.

- 1 to 2 years stable: Graded simplified coverage at a few select carriers.

- 2 or more years stable: Standard simplified approval at multiple companies.

A single stent past the five-year mark is barely noted by underwriters. Multiple stents or repeat bypass procedures trigger much stricter handling.

We help clients gather the right medical records to prove their post-surgery stability. Securing life insurance with stent placement requires showing a consistent track record of follow-up care. Consistent medical care proves to the insurer that you take your health seriously.

Medication-List Considerations

We always review your prescription history before recommending a specific policy. Carriers run an automatic check through the national prescription database during underwriting. Medications that signal routine cardiac care show the insurer that you are managing your health.

Our favorite carriers view maintenance drugs as a positive signal rather than a penalty.

- Routine Maintenance: Statins, beta-blockers, and ACE inhibitors are standard and expected.

- Blood Thinners: Anticoagulants like Warfarin or Eliquis are generally acceptable for stable patients.

- Red Flag Additions: Recent prescriptions for nitrates usually signal new chest pain.

- Advanced Warning Signs: Digoxin indicates more advanced congestive heart failure.

Several new medications added in the past few months suggest an unstable clinical picture. This pattern will almost certainly cause an underwriter to pause or decline the application.

We always verify your exact drug list to match you with the most forgiving insurance company. Finding a carrier that understands your specific prescriptions saves you money.

When Guaranteed Issue Makes Sense

Our clients with recent cardiac events often need an alternative solution for immediate coverage. Recent events within the last 12 months usually point directly to guaranteed issue coverage. Congestive heart failure or multiple major health conditions also fall into this category.

We recommend these policies because they require no medical exams and ask zero health questions. The tradeoff is a higher monthly premium and a strict two-year graded benefit period. If a natural death occurs during those first two years, the carrier refunds your premiums plus an interest rate typically around 10 percent.

Our data from 2026 shows that most guaranteed policies cap the maximum death benefit at $25,000. This maximum limit provides just enough funding to cover standard funeral expenses and immediate outstanding bills. The chart below illustrates the main differences between coverage types.

| Feature | Simplified Issue | Guaranteed Issue |

|---|---|---|

| Health Questions | Yes | No |

| Waiting Period | None (Day One Coverage) | 2 Years (Graded Benefit) |

| Maximum Coverage | Up to $40,000 or $50,000 | Usually Capped at $25,000 |

| Monthly Pricing | Lower Cost | Higher Cost |

The Practical Path

We find that simplified issue is highly realistic for stable applicants past the one-year mark. Choosing the right A-rated carrier makes a massive difference in your final monthly price. Recent 2026 industry data shows the average cost of a $10,000 final expense policy is roughly $74 per month for a 60-year-old.

Our agents frequently quote Mutual of Omaha and Transamerica for burial insurance heart disease policies. Mutual of Omaha offers lower rates for healthy applicants but asks very strict medical questions. Transamerica accepts paired conditions like diabetes with cardiac history but typically costs 20 to 35 percent more. If diabetes is part of your picture, our guide to Burial Insurance for Diabetics explains how carriers weigh that second condition.

We recommend consulting an independent agent who handles complex cardiac cases every single day. An experienced professional knows exactly which companies underwrite your specific history most favorably. That specific knowledge saves you from unnecessary declines and locks in the lowest possible rate to protect your family.

Moving Forward With Confidence

Our priority is making sure your property and business assets remain secure. Finding affordable life insurance after a heart attack is entirely possible with the right strategy. You now have the facts to make a smart, informed decision.

We encourage you to review your recent medical records and verify your medication list. Compare the A-rated carriers we discussed to secure the best possible rate. Taking action today guarantees your family will not face a financial burden later.