We know securing life insurance with COPD presents a major challenge. Most property owners assume a chronic breathing condition means automatic rejection. This assumption costs families crucial financial protection every single day.

According to the American Lung Association, over 11 million adults in the US live with a diagnosed respiratory issue. This 2025 data shows just how common this situation is.

Insurers process these specific applications constantly.

Our team regularly observes that approval comes down to presenting the right medical details to the right underwriter. Let’s look at the data, what it actually tells the insurance carriers, and explore a few practical ways to respond.

The Spectrum Matters

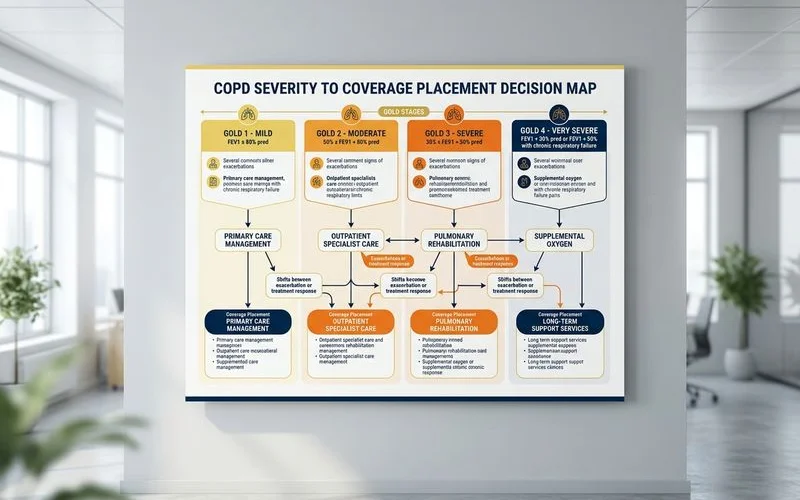

Your position on the COPD severity spectrum directly determines the life insurance rates and coverage types available to you. Insurers classify the disease into four main stages, ranging from mild, well-managed cases to advanced situations requiring continuous oxygen.

We look at clinical markers like your Forced Expiratory Volume (FEV1) score to predict how underwriters will view your application. A high FEV1 score indicates better lung function, which opens the door to standard pricing.

The Global Initiative for Chronic Obstructive Lung Disease (GOLD) system also helps carriers gauge your exact risk level. This clinical data shapes your path forward. The most useful mental model is a four-stage breakdown:

| COPD Stage | Typical Profile | Expected Coverage Path |

|---|---|---|

| Mild | No oxygen use, no recent hospitalizations, high FEV1 score. | Often qualifies for simplified issue at standard or graded rates. |

| Moderate | Inhaler-controlled, occasional flare-ups, moderate FEV1. | Usually graded simplified issue at most major carriers. |

| Advanced | PRN (as-needed) oxygen, frequent ER visits. | Graded simplified at a few carriers, or Guaranteed issue. |

| Severe | Continuous oxygen, recent hospitalizations. | Guaranteed issue is the realistic and appropriate answer here. |

What Carriers Ask About

A typical simplified-issue application asks about your exact diagnosis date, oxygen use, recent hospitalizations, steroid treatments, and smoking history. These specific questions help the carrier calculate your precise mortality risk within minutes.

We often notice applicants are surprised by how closely insurers scrutinize prescription records. Underwriters pull a digital pharmacy report to verify the exact inhalers and corticosteroids you use.

A “yes” to any knockout question routes you out of simplified issue at that specific carrier. Continuous oxygen use or a hospital stay within the last 12 months almost always triggers an automatic decline for standard coverage.

The Core Underwriting Questions

Carriers vary significantly in what they consider a knockout. One insurer will decline an application based on continuous oxygen, while another offers a graded benefit.

Here are the specific details you must prepare to answer:

- Current COPD diagnosis and the exact date.

- Oxygen use (none, as-needed, or continuous).

- Hospitalizations in the past 12 to 24 months.

- Steroids or other treatment for flare-ups in the past year.

- Smoking history (current, former, never).

- Other respiratory conditions like emphysema, chronic bronchitis, or asthma.

This variance in knockout criteria makes shopping multiple carriers worth the effort. You need a strategy built for your specific medical history.

Lenient vs Strict Carriers

Lenient carriers specialize in the senior market and offer graded policies, while strict carriers route any life insurance breathing condition case directly to guaranteed issue. These internal guidelines shift frequently based on the insurer’s financial goals.

We track these underwriting changes closely to protect our clients from unnecessary rejections. A carrier that approved moderate COPD at standard rates in 2025 might tighten their rules in 2026.

Insurers generally fall into two categories:

- Lenient carriers typically have larger senior-market specializations and offer graded simplified issue more often.

- Strict carriers route COPD applications quickly to guaranteed issue, even for milder cases.

An independent agent who handles respiratory cases regularly knows which carriers currently take COPD applicants more leniently. This knowledge shifts every few quarters as carriers adjust their substandard rating tables. Finding the right match prevents a permanent decline on your record.

When Guaranteed Issue Becomes the Right Call

Guaranteed issue is the right call when continuous oxygen, advanced disease, or recent hospitalizations make standard approvals impossible. This product skips all health questions to ensure you secure immediate coverage.

We consider this path a highly practical solution rather than a failure. The policy has a higher premium, but it puts concrete financial protection in place for your family.

According to recent data from the National Funeral Directors Association, the median cost of a US funeral is approximately $8,300. Many people use a guaranteed issue policy as a primary form of burial insurance for COPD. These policies typically max out around $25,000 in total coverage, which easily handles those final expenses.

Before signing the paperwork, you should understand how the standard graded benefit period functions:

- Years 1 and 2: Non-accidental deaths result in a refund of premiums paid, plus 10% to 30% interest.

- Accidental Deaths: The full coverage amount is paid immediately, regardless of the timeline.

- Year 3 and Beyond: The full death benefit pays out for any cause of death.

This is the product working exactly as intended for a specific clinical situation. The primary goal is to establish reliable coverage that matches your actual underwriting profile.

The Practical Path

The practical path requires working with an independent professional to shop multiple A-rated carriers in parallel. This coordinated approach protects your medical background file while finding the best available rate.

We strongly warn property owners against applying randomly online. The Medical Information Bureau (MIB) tracks life insurance application data in the US for up to seven years.

Multiple rapid declines generate warning codes on your MIB report.

These codes can complicate later applications at entirely different companies. If a carrier has already turned you down, our guide on being Declined for Life Insurance? What to Do Next explains how to re-shop without stacking up more flags. A coordinated strategy looks like this:

- Talk to an independent agent who can shop simplified issue at 3 to 5 A-rated carriers in parallel.

- Apply where the agent thinks your profile fits best, based on current carrier tables.

- If simplified issue isn’t realistic, move to guaranteed issue at a carrier with a 2-year graded period (preferable to 3 years).

A good agent sequences your applications properly to avoid triggering these database red flags. Reach out to a licensed professional today to start comparing quotes safely.