What “Rated Up” Means

When a carrier rates up your application, they’re issuing the policy at a higher-than-standard premium because they assess your risk as elevated. The surcharge is expressed as a “table rating” (Table 1 through Table 8 or A through H, depending on carrier convention) or as a flat percentage above standard.

Each table typically adds roughly 25% to the standard premium:

- Table 1 / A: ~25% above standard

- Table 2 / B: ~50% above standard

- Table 4 / D: ~100% above standard

- Table 8 / H: ~200% above standard

A 65-year-old male whose standard rate would be $80/month for $10,000 might get rated Table 2 at $120/month. Over 15 years, that’s $7,200 in extra premium for the same coverage.

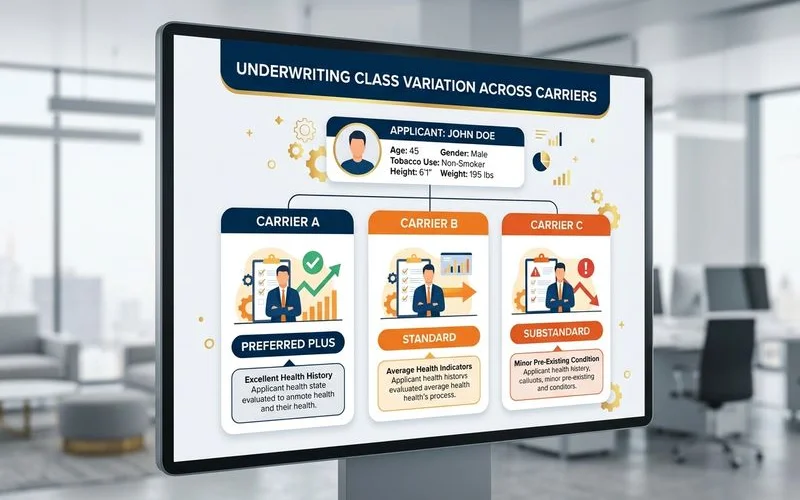

Why the Same Person Lands in Different Classes

Underwriting tables aren’t standardized across carriers. Carrier A’s algorithm might place your condition in a different table than Carrier B’s, even though you’re the same person with the same medical history.

For example, the carrier spread on burial insurance for diabetics is wide: well-controlled Type 2 diabetes on metformin might be:

- Standard rates at Carrier A

- Table 2 at Carrier B

- Decline at Carrier C

- Preferred at Carrier D (specialized in diabetic underwriting)

The “right” carrier for you is the one whose table is friendliest to your specific profile. That’s almost never visible from the outside — and almost never the carrier that’s been advertising at you.

The Dollar Impact Over Time

A rated-up offer feels acceptable in the moment because it’s still coverage. But the math gets ugly over 10–20 years:

| Standard | Table 2 (50% up) | 15-Year Difference |

|---|---|---|

| $80/mo | $120/mo | $7,200 |

| $100/mo | $150/mo | $9,000 |

| $120/mo | $180/mo | $10,800 |

That’s real money — and it’s the cost of accepting the first offer without shopping. Most people don’t realize they’re paying for it because the surcharge is just labeled as their premium.

How to Request a Re-Comparison

If you’ve been rated up and want to shop the same case at other carriers:

- Get the underwriting decision in writing. You’re entitled to know which condition triggered the rating.

- Don’t immediately accept the offer. You typically have a window (often 30–60 days) before the offer expires.

- Talk to an independent broker who handles your condition type regularly. Ask which 2–3 alternative A-rated carriers have friendlier tables for that condition.

- Apply with one carrier at a time (avoid simultaneous applications that can complicate underwriting via MIB).

- Compare the offers side by side. The right one is usually obvious.

If no carrier offers better than the original rated-up class, the first offer was actually appropriate for your situation — that’s useful information too. But you won’t know until you’ve checked.

The Soft Bridge

Independent brokers exist for exactly this situation. Captive agents can only offer one company’s table. Independents shop the field. If you’re staring at a rated-up offer that feels high, the second opinion is free — and often substantially cheaper.