A Plain Definition

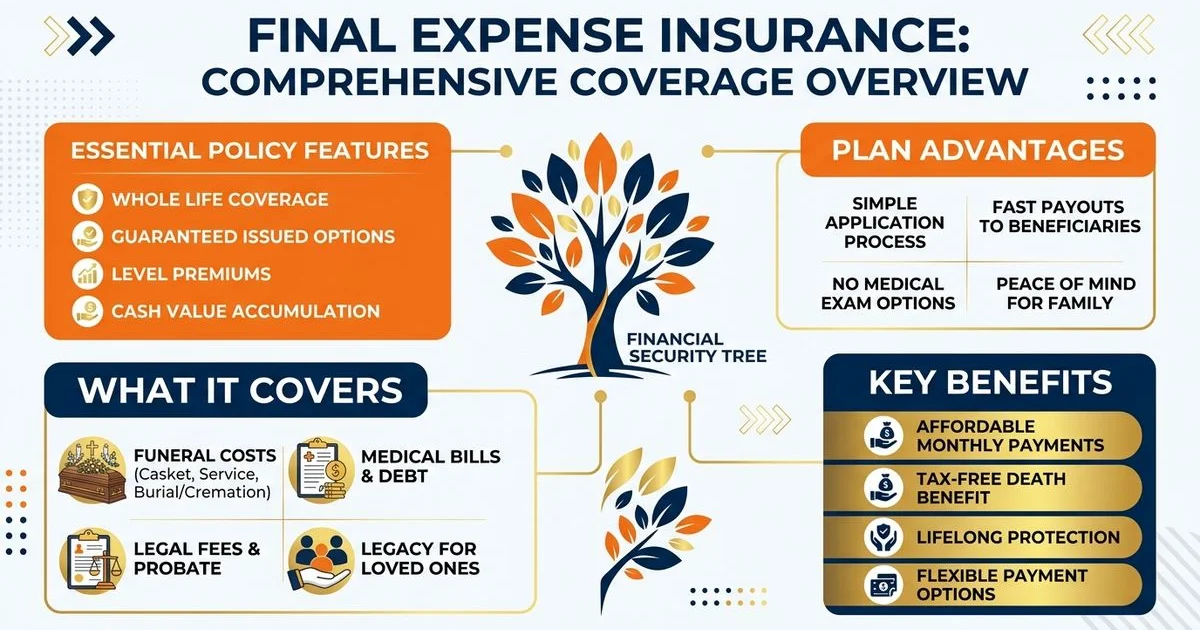

Final expense insurance is a small whole-life policy designed to cover the costs that follow a death — funeral services, burial or cremation, outstanding medical bills, and small consumer debts. Coverage amounts typically range from $5,000 to $35,000, and the death benefit pays directly to your named beneficiary as a tax-free lump sum.

It’s sometimes called burial insurance, funeral insurance, or simplified-issue whole life. They all describe the same product, just with different marketing labels. What matters is the underlying mechanics: it’s permanent coverage, the premium doesn’t go up, and the benefit doesn’t decrease.

What It Actually Pays For

The beneficiary receives a check, and they decide how to spend it. There are no restrictions. Common uses include:

- Funeral services (casket, embalming, viewing, transportation)

- Burial costs (plot, vault, headstone, opening/closing fees)

- Cremation services (direct or with memorial)

- Outstanding medical bills not covered by Medicare or insurance

- Small consumer debts the family doesn’t want to inherit

- Travel costs for family attending the service

A typical funeral with burial in the United States now runs $10,000 to $15,000 or more, and a traditional service with cremation isn’t far behind. Direct cremation is significantly cheaper — sometimes under $2,000 — which changes how much coverage you actually need.

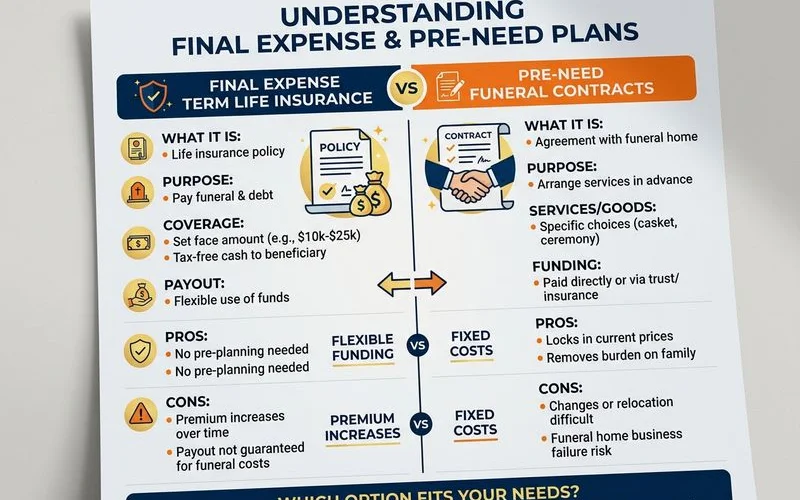

How It Differs From Term Life and Pre-Need Contracts

Term life insurance covers you for a fixed period (10, 20, or 30 years). If you outlive the term, the coverage expires with no payout. Term life is designed to replace income, not to cover end-of-life costs. Most people who buy final expense have already outlived any term policy they once had.

Pre-need funeral contracts are bought directly from a funeral home and prepay for specific funeral services. They lock in services at today’s prices but tie the money to that particular funeral home — if the home goes out of business or you move states, the contract can become difficult to use. A final expense insurance policy is portable and pays cash, not services.

Final expense whole life is permanent (doesn’t expire), pays cash (not services), and the premium is locked in for life. That’s why it’s the dominant choice for end-of-life coverage.

Who It’s For

Final expense is sized and priced for adults aged 50 to 85 who want to make sure their funeral and burial don’t become a financial burden on family. Coverage is permanent, premiums don’t increase, and approval is based on a short health questionnaire (or no questions at all, for guaranteed issue).

If you’re younger or have higher income-replacement needs, term life or a larger whole life policy is usually a better fit. Final expense is purposefully small, simple, and built for the specific job of covering end-of-life costs.

Bottom line: Final expense insurance is a small permanent whole life policy designed to make sure end-of-life costs don’t land on your family. Coverage typically ranges from $5,000 to $35,000 and pays as a tax-free lump sum.

What’s Next

Once you know what the product is, the practical questions follow: how much will it cost, which carriers should you compare, and which underwriting tier fits your health profile. The underwriting-tier guide walks through preferred, simplified, graded, and guaranteed in plain language. For real-world price ranges, see the cost guide.

Most people don’t shop final expense more than once. Get it right the first time — and that starts with understanding what you’re actually buying.